To appreciate why efficiencies driven by information are crucial to the banking sector, let us do some number crunching. Note: All data below are results of Probe research.

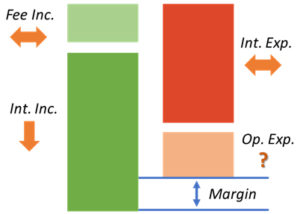

Broadly speaking, banks’ income can be categorized into interest income (interest on loans to borrowers) and non-interest income (fees and commissions, profits from trading, etc.). On the expense side, we have interest expense (interest paid on deposits), and operating expenses (sales and marketing, legal fees, credit and risk analysis, employee compensation and benefits, etc.).

So to get a sense of a bank’s margin spread, we can look at:

Spread = ( InterestIncome/TotalFunds + (Non-InterestIncome)/TotalFunds ) – (InterestExpense/TotalFunds + OperatingExpense/TotalFunds)

Let’s see what the data is telling us. We will use consolidated data on all major Indian banks over the last 25 years, starting at 1992, right after liberalization.

Here is how interest income is trending over this quarter-century:

Over the course of the ‘90s, interest income began trending upwards, reaching a high-point of 11.22 in 1997. Over the ‘00s and ’10s, this metric stabilized, with a gradual trend downward. In 2016, interest income to total funds stood at 8.44.

Over the next few decades, interest income will continue to trend marginally downward; loans will get repaid or renegotiated at lower rates as the economy matures. While the Indian market still has sufficient room to grow until it reaches maturity, the end state is inevitable — interest income growth will not keep rocketing upward.

Non-interest income (primarily fees) has meanwhile remained steady at around the 1 mark over the last 10 years. In fact, it has declined from its high point of 2+ in the mid-00s. Indian banks still are quite heavily dependent on interest income, and have not diversified their income streams to the extent that banks in advanced economies have.

Now let us look at the expenses:

Interest expenses, which fluctuate depending on rate cuts and hikes by the RBI, have centered around the 6-mark.

Over the 90s’ and 00’s, operating expenses were brought down from around 3.5 to about 2. This was due to efficiency-improving factors such as information technology. Over the last decade, though, operating expenses have remained flat.

Let us now merge the 2 pictures to look at the margins over these 27 years:

As you can see, incomes and expenses have been moving up and down more or less in tandem over the last two and a half decades. But with interest incomes trending gradually downward, with all else being the same, margins begin to get squeezed in the coming years.

In such a scenario, how will banks ensure they maintain (and improve) their spreads? How do they stay above water?

They have two levers at their disposal — increasing non-interest incomes, and decreasing operating expenses.

The first of the two — increasing fee and other non-interest incomes — is quite limited in the amount of heft it can provide. The increased competitiveness of the financial services marketplace — and hence the market’s price sensitivity — places hard limits on this lever. Which leaves us with the second option — reducing operating expenses.

To remain competitive and profitable, banks need to launch a new wave of efficiency enhancements. While the earlier wave (in the ‘90s and ‘00s) was driven by systems integration and the Internet, the next round will be driven by data and analytics.

With easy access to relevant and rich data, banks can drastically improve targeting and decrease cycle times across the board, whether in sales or credit disbursement. Data can drive accurate credit and risk analysis, bringing down the proportion of NPAs. High-quality on-demand information can drive down customer acquisition costs. Portals and APIs can load data automatically into credit models to display rating scores in seconds. In the long run, data will enable sharper targeting and predictive analytics, which will not just bring down costs but also propel growth.

In summary, to stay competitive, banks need to reduce OpEx; and to reduce OpEx, banks need data.

Closing the Information Gap

The need of the hour is for on-demand information on Indian companies — information that is comprehensive, validated, and clean. Sales, credit, and risk teams need to base their decisions on hard data; they need to expand their models to incorporate information on companies’ legal history, defaulting history, directors’ track records, etc. They need to understand the connections between companies — via common directors or owners, for instance — to estimate risk and foresee ripple effects.

The path to a more profitable and sustainable future for banking in India is paved with data and analytics. Ultimately, closing the information gap will result in a fairer and more competitive marketplace, and will power us toward a better India. And that is exactly the vision that Probe Information Services is working toward.