In Brief: India’s debt recovery landscape is more complex and revealing than most financial analyses capture. A Probe42 study of litigation data across Indian courts uncovers over 60,000 recovery cases amounting to ₹1.9 lakh crore in claims. These cases, spread across District Courts, Commercial Courts, Debt Recovery Tribunals (DRTs), and the National Company Law Tribunal (NCLT), highlight where financial distress first surfaces, often months before it appears in financial statements or credit reports. For banks, NBFCs, investors, and compliance professionals, understanding this court ecosystem is key to identifying early warning signs, evaluating counterparties, and mitigating credit and operational risk.

The Expanding Footprint of Recovery Litigation in India

Litigation data provides a real-world pulse on financial stability. Unlike traditional risk metrics, court filings reveal when and where financial disputes originate, long before defaults become public.

Across India, tens of thousands of companies are currently engaged in debt-related litigation, with total claims crossing ₹1.9 lakh crore.

- District & Sessions Courts: 5,300+ cases worth ₹57,978 crore

- Senior Civil Judges/Lower Courts: 2,500+ cases worth ₹2,703 crore

- Commercial Courts: Over ₹5,300 crore in disputes

- Tribunals (DRTs, NCLTs): Account for most of the large-value recovery and insolvency cases

The sheer distribution of cases shows how financial stress percolates through multiple layers of India’s judicial system, from small operational defaults to high-value insolvency proceedings.

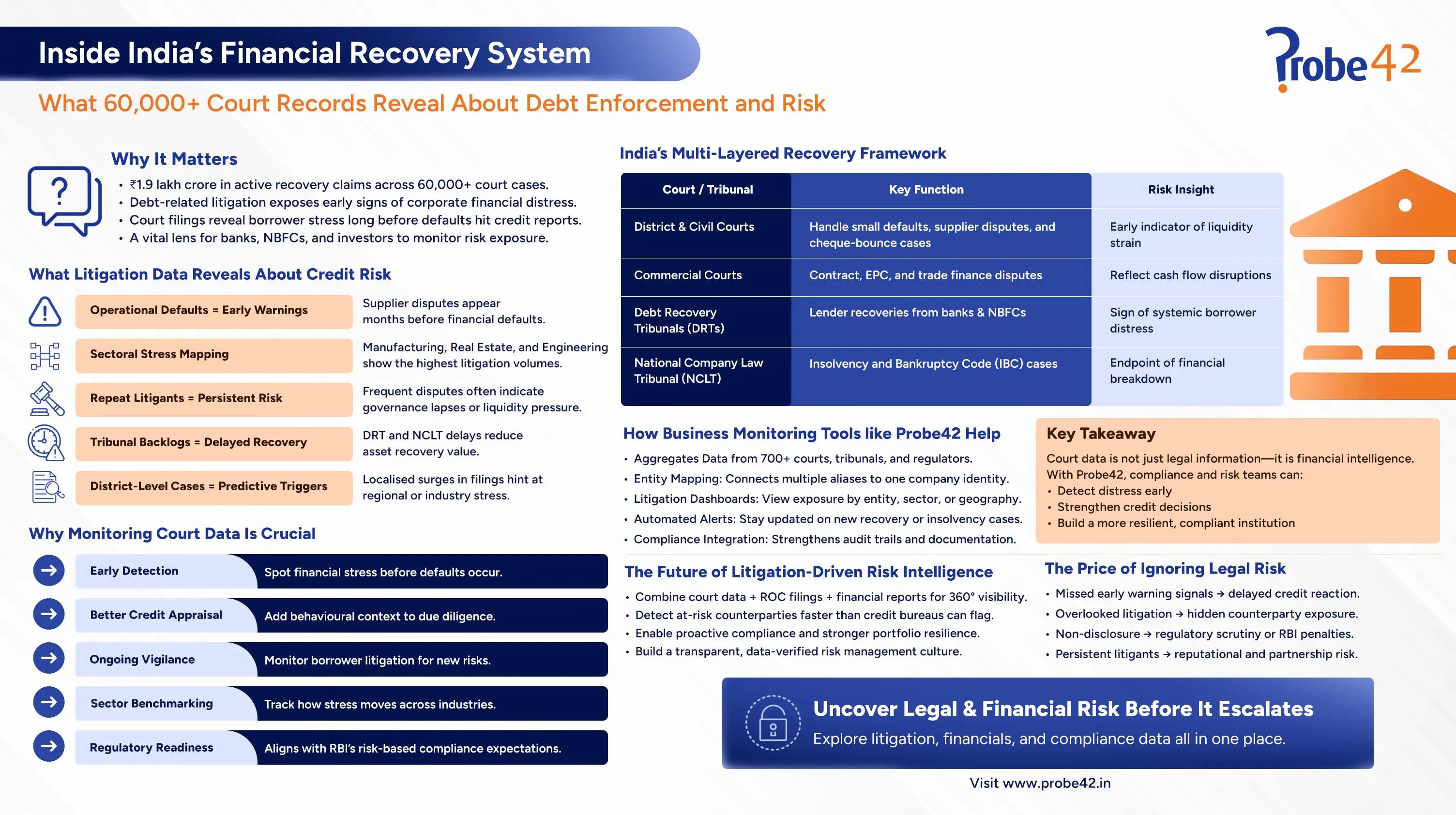

India’s Multi-Layered Recovery Framework

1. District and Civil Courts: The First Signs of Stress

District and lower civil courts are the first touchpoints for operational defaults, typically supplier disputes, unpaid invoices, and cheque-bounce cases. Because these courts are more accessible and less expensive to approach, small and medium businesses often file here first, making this ecosystem an early barometer of liquidity strain in the economy.

Key Takeaway: Rising case volumes at this level can signal mounting pressure on working capital cycles well before larger financial defaults occur.

2. Commercial Courts: The Mid-Tier Dispute Layer

Commercial Courts handle structured, high-value contract disputes—construction delays, EPC contracts, service defaults, and trade finance disagreements. These cases usually involve larger corporates or consortiums and have direct implications on creditworthiness, since unresolved commercial suits can delay receivables and distort balance sheets.

Insight: Entities frequently appearing in commercial disputes tend to show volatility in cash flows and delayed supplier settlements.

3. Debt Recovery Tribunals (DRTs): The Core of Lender Enforcement

DRTs were set up specifically for the recovery of debts owed to banks and financial institutions. Cases filed here indicate that defaults have escalated from civil disputes to formal lender recovery actions. With over ₹8 lakh crore in cases pending, DRTs form the backbone of India’s financial enforcement network.

Insight: A borrower’s appearance in DRT records is a major risk trigger; it indicates systemic liquidity issues or severe borrower-bank disputes.

4. National Company Law Tribunal (NCLT): The Insolvency Endpoint

NCLT handles cases under the Insolvency and Bankruptcy Code (IBC), including both financial creditor petitions (Section 7) and operational creditor claims (Section 9). With cases valued above ₹8 lakh crore, NCLT reflects India’s most distressed corporate cases. Its filings help credit teams assess sector-wide insolvency trends and the efficiency of debt resolution under IBC.

Observation: As operational defaults rise, NCLT filings follow within quarters, making the linkage between early operational stress and eventual insolvency clear.

What Litigation Patterns Reveal About Credit Risk

1. Operational Defaults Lead Financial Distress:

Supplier disputes, delayed payments, and cheque-bounce cases appear far earlier than loan defaults. These operational disputes are often the first ripple of financial instability, signalling cash flow tightening within companies. For lenders and investors, monitoring such patterns helps identify which businesses are struggling to meet day-to-day obligations before larger credit exposures turn risky.

2. Sectoral Stress is Traceable and Quantifiable:

Litigation trends reveal stress hotspots. Manufacturing, real estate, and engineering sectors consistently show the highest volume of recovery filings. This concentration is not random; it mirrors working capital bottlenecks, project delays, and cyclical downturns in these industries. By tracking sector-wise litigation intensity, institutions can predict where credit deterioration may cluster next.

3. Repeat Litigants Drive Risk Concentration:

A small number of corporates are involved in dozens of active cases simultaneously—either as defendants or plaintiffs. These “repeat litigants” indicate systemic governance or liquidity issues. Persistent disputes also suggest poor counterparty management or unresolved structural weaknesses that make the entity a long-term risk.

4. Tribunal Overload Reflects Systemic Stress:

DRT and NCLT backlogs reveal that while India’s regulatory framework is robust, enforcement remains slow. Prolonged litigation often erodes asset value and recovery prospects. For financial institutions, understanding where claims are stuck and how long resolutions typically take helps refine recovery expectations and provisioning strategies.

5. District-Level Filings as Predictive Triggers:

District and civil courts offer granular insights into early-stage defaults. A sudden spike in filings within a region or cluster can point to localised liquidity issues or sector-linked stress. These micro-patterns, when aggregated nationally, provide predictive intelligence for macro-level portfolio management.

From Data to Insight: Why Monitoring Courts Matters

1. Early Detection of Financial Distress:

Court records serve as an early-warning radar for lenders and investors. When suppliers or creditors initiate recovery suits, it is an immediate signal of strain in payment cycles. Tracking these disputes helps institutions act before defaults appear in financial reports; adjusting exposure, collateral, or repayment structures in time.

2. Strengthened Credit Appraisal and Counterparty Screening:

Traditional financial due diligence offers a snapshot, not a storyline. Litigation intelligence adds context—revealing whether a company has a pattern of delayed payments, unresolved legal disputes, or frequent contract terminations. Integrating this insight into appraisal workflows strengthens decision-making and reduces the onboarding of high-risk entities.

3. Continuous Portfolio Vigilance:

Once credit is extended, ongoing monitoring is crucial. Real-time tracking of litigation across courts provides dynamic risk visibility. If a borrower suddenly faces multiple recovery cases, lenders can trigger internal reviews, adjust risk ratings, or initiate restructuring measures proactively.

4. Peer and Sector Benchmarking for Strategic Positioning:

Analysing aggregated litigation data across industries enables comparative benchmarking. For example, if litigation exposure in the real estate sector doubles within a quarter, it signals systemic stress that may influence related sectors like cement or construction finance. This intelligence helps investors and banks rebalance portfolios before contagion spreads.

5. Compliance, Audit, and Regulatory Strengthening:

With the Reserve Bank of India tightening expectations around credit and operational monitoring, litigation data serves as verifiable evidence of oversight. It helps compliance teams demonstrate continuous due diligence, reinforces audit readiness, and aligns institutions with regulatory best practices under RBI’s risk-based supervision frameworks.

Leveraging Business Monitoring Tools for Smarter Risk Detection

While litigation data is public, manually tracking court filings across hundreds of jurisdictions is impossible. Business monitoring platforms like Probe42 solve this by automating data extraction, entity mapping, and red flag generation.

Here is how they add value:

1. Unified Data Collection: Aggregation of records from 700+ courts, tribunals, and regulators ensures complete visibility into a company’s legal exposure.

2. Entity Resolution and Standardisation: Probe42 uses AI-based entity matching to connect cases across jurisdictions, ensuring multiple name variations are tied to the same business.

3. Sectoral Benchmarking Dashboards: Litigation data can be visualised at the sector or industry level, helping financial institutions compare their exposure to systemic trends.

The Price of Ignoring Legal Risk

Compliance and credit teams that overlook litigation data often face downstream consequences:

- Delayed Reaction to Credit Deterioration: Defaults appear “sudden” only because warning signals in court data went unnoticed.

- Hidden Counterparty Exposure: A borrower or vendor entangled in multiple suits can disrupt repayment chains or supply contracts.

- Reputational Risk: Association with litigation-heavy counterparties affects investor confidence.

- Regulatory Penalties: Failing to detect or disclose litigation exposure may attract supervisory observations under RBI’s compliance frameworks.

In short, ignoring court data leaves banks and corporates reactive rather than prepared.

Building the Future of Litigation-Driven Risk Intelligence

India’s courts collectively process tens of thousands of financial recovery suits every year, forming the most direct reflection of corporate stress. The challenge is not a lack of information; it is fragmentation. To stay ahead, institutions must integrate judicial data with financial, operational, and compliance analytics.

With platforms like Probe42, this integration is no longer theoretical—it is practical and scalable. By connecting data across ROC filings, litigation records, and financial statements, Probe42 enables:

- Early identification of risky counterparties

- Real-time portfolio monitoring

- Enhanced due diligence and onboarding workflows

- Continuous compliance visibility

Conclusion: Data-Driven Vigilance is the New Compliance

India’s financial recovery landscape is a mirror of its corporate health—dynamic, diverse, and data-rich. Court records reveal stories that balance sheets cannot: supplier disputes that predate defaults, credit recoveries that reshape sectors, and insolvencies that define lending cycles.

For risk professionals, the message is clear: litigation intelligence is not an accessory; it is an advantage. By embedding it into credit, compliance, and due diligence frameworks, organisations can detect distress early, protect portfolios, and build resilient, transparent financial ecosystems.

Frequently Asked Questions (FAQs)

1. How does court litigation data help in credit risk assessment?

Court filings act as real-time indicators of financial stress. When companies face multiple recovery or operational disputes, it often signals tightening liquidity or governance lapses. Tracking litigation data helps lenders and investors identify high-risk entities before defaults appear in financial statements.

2. Why should banks and NBFCs monitor district and commercial court cases?

District and commercial courts capture the earliest signs of financial friction—delayed payments, supplier disputes, or contract breaches. These cases surface months before NCLT or DRT proceedings, giving risk and compliance teams a crucial head start in detecting potential defaults.

3. How can platforms like Probe42 improve legal risk monitoring?

Probe42 aggregates data from 700+ Indian courts and tribunals, standardises it, and links it with company financials. This allows banks, NBFCs, and investors to monitor ongoing disputes in real time, benchmark sectoral risk, and strengthen due diligence and compliance workflows.