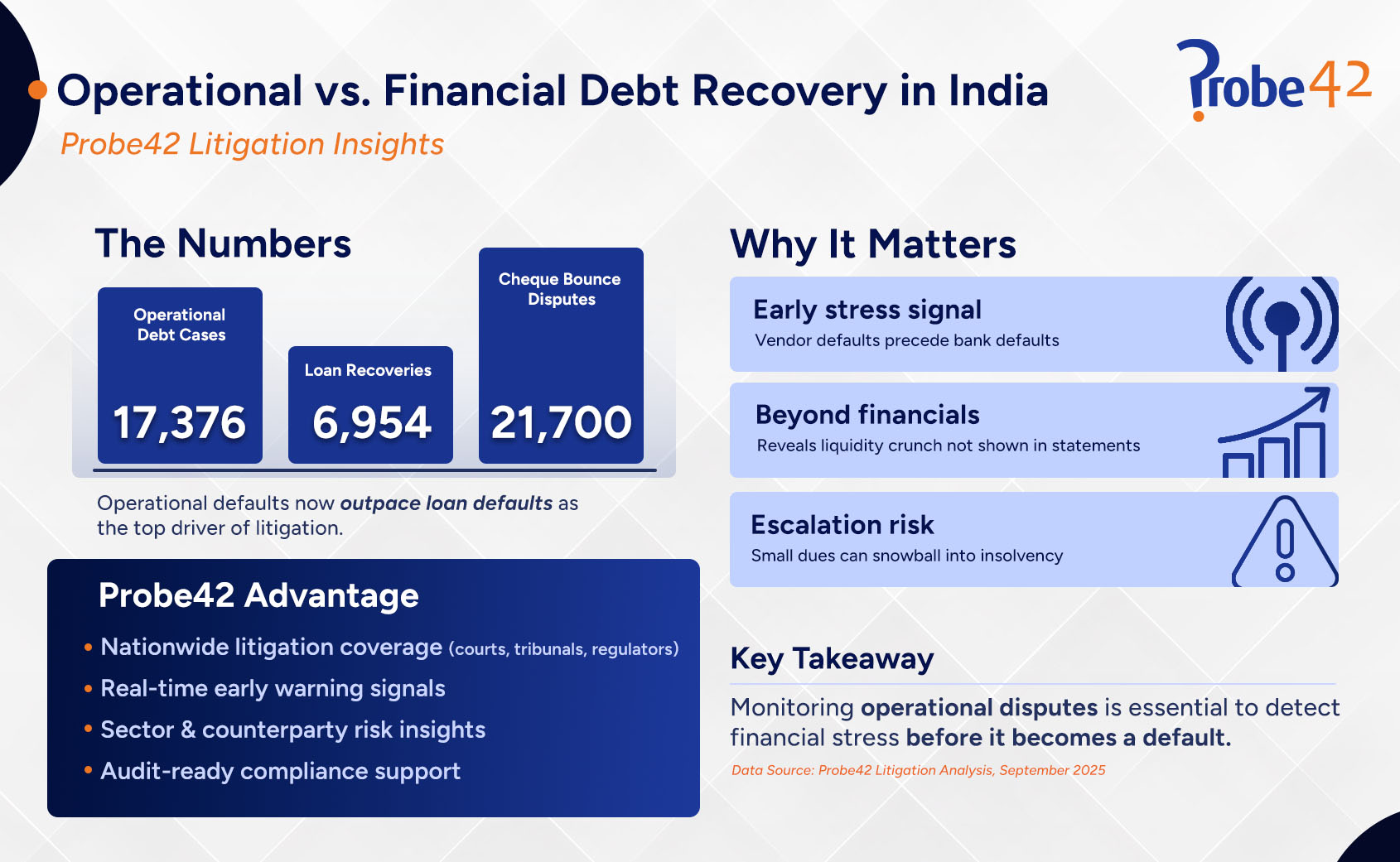

In Brief: Operational debt recovery has overtaken financial loan recovery as the leading driver of litigation in India. Probe42’s analysis shows over 17,000 operational debt cases compared to 6,900 loan recoveries, with cheque bounce disputes adding another 21,700 cases. This trend signals that vendor and supplier defaults are now key indicators of financial stress, often surfacing before bank loan defaults. For risk, credit, and compliance teams, monitoring operational disputes is essential to building accurate risk profiles and detecting early warning signals.

====

When most people think about debt recovery in India, the immediate association is with loan defaults, SARFAESI proceedings, and financial creditors. But litigation data tells a different story. Probe42’s aggregated insights reveal that operational debt recoveries have overtaken financial loan recoveries as the leading cause of corporate recovery cases in India.

This shift is more than a statistic—it represents an important early-warning signal for lenders, compliance teams, and businesses. Operational defaults, such as unpaid supplier or vendor dues, often surface well before a company defaults on bank loans, making them critical to monitor.

Understanding Debt Recovery in India

To understand the implications of this trend, it is important to distinguish between the two types of recoveries:

Financial Debt Recovery: Linked to loans and credit facilities provided by banks and financial institutions. These cases are typically filed under SARFAESI or NCLT Section 7.

Operational Debt Recovery: Stemming from payments owed for goods and services supplied. Vendors, suppliers, and contractors often file these cases, usually under NCLT Section 9.

Traditionally, financial debt recovery has dominated discussions around risk and compliance. However, operational debt disputes are increasingly shaping the litigation landscape.

Probe42 Litigation Data: The Shift in Numbers

Probe42’s litigation analysis highlights a significant change in debt recovery trends:

- Operational Debt Recoveries: 17,376 cases filed

- Loan Recoveries: 6,954 cases filed

- SARFAESI Cases: 3,948

- Cheque Bounce Cases: 21,700 (many directly linked to unpaid vendor payments)

- Excess Payment Recovery: 9

- Damage Recovery: 12

Key Takeaway: Operational debt recovery alone now makes up more than 35% of litigation cases filed by companies in Indian courts. When factoring in cheque bounce disputes, the share of operational defaults becomes even more dominant.

Why Are Operational Debt Recoveries Surging?

1. Delayed Vendor and Supplier Payments:

Many businesses, especially those operating with tight margins, are increasingly delaying vendor and supplier payments to manage cash flow pressures. While these delays may seem minor, they are leading to a substantial rise in disputes. Vendors, who often operate with limited working capital, cannot afford long payment cycles, resulting in quicker escalation to litigation. This trend reflects both financial strain in corporates and the growing unwillingness of suppliers to tolerate defaults.

2. Growing Legal Assertiveness Among SMEs:

In the past, small and mid-sized enterprises (SMEs) were reluctant to pursue litigation due to cost, time, and the belief that recovery through legal means was uncertain. Today, the environment has shifted. SMEs are far more assertive, using structured legal mechanisms to enforce payments. The Insolvency and Bankruptcy Code (IBC) has made operational creditors more confident about approaching tribunals, particularly under Section 9, which allows even smaller disputes to be escalated to insolvency proceedings.

3. Increased Use of NCLT Section 9:

Section 9 of the IBC, dedicated to operational debt recovery, has become the go-to provision for suppliers and contractors. The availability of this legal route has lowered the barrier for operational creditors to demand repayment. Its design, which allows operational creditors to trigger insolvency if dues remain unpaid, makes it a powerful tool, and its use is now reflected in the sharp increase in case volumes.

4. District Courts as Recovery Hubs:

While tribunals like the NCLT and DRT receive more attention, district courts have quietly become central to recovery litigation. Thousands of operational disputes are filed every year at this level, often by smaller businesses and local suppliers. The accessibility and lower costs of filing cases in district courts have made them a preferred channel for operational creditors. This makes the district judiciary an often-overlooked but critical piece of India’s recovery ecosystem.

5. Operational Stress as a Broader Economic Indicator:

The rise in operational debt disputes is also symptomatic of larger economic realities: lengthening payment cycles, stress in supply chains, and uneven recovery across sectors. These disputes often reveal early stress signals across industries like manufacturing, real estate, and services, where delayed payments are common. This means operational debt recoveries are not just isolated legal actions—they are a barometer of wider financial strain in the economy.

Why This Matters for Risk and Compliance Teams

1. Early Warning of Financial Stress:

Operational defaults typically precede financial loan defaults. A company that is unable to pay vendors on time today could struggle with larger financial obligations tomorrow. For risk and compliance professionals, monitoring operational disputes provides a crucial early-warning system to anticipate defaults.

2. Exposure Beyond Financial Statements:

Traditional due diligence often focuses on balance sheets and loan repayment history. However, operational debt disputes expose liquidity problems and cash flow mismatches that financial statements may not immediately reveal. Ignoring these disputes can mean missing vital signs of stress.

3. Escalation into Insolvency Proceedings:

What begins as a small operational dispute can quickly escalate. Multiple cases, if left unresolved, may lead to insolvency petitions under the IBC. This can cause reputational harm, loss of supplier trust, and heightened regulatory attention. Risk teams need to account for this escalation path in their assessments.

4. Holistic Risk Profiling:

Operational litigation should be integrated into credit and compliance models alongside financial disputes. By considering both, institutions gain a more holistic view of corporate health. This enables more accurate risk scoring, reduces onboarding risks, and strengthens decision-making frameworks.

5. Sectoral and Counterparty Monitoring:

Certain industries, such as manufacturing, real estate, and services, are more prone to operational defaults. By monitoring trends at a sectoral level and identifying counterparties frequently involved in such disputes, compliance teams can proactively flag high-risk entities. This ensures institutions are not blindsided by systemic risks in vulnerable sectors.

How Probe42 Strengthens Debt Recovery Monitoring and Risk Assessment

Traditional financial analysis often misses the early signals of operational stress. By the time defaults appear in loan repayments, the damage has already spread across vendors, suppliers, and counterparties. Probe42 bridges this gap by giving organisations a complete view of both financial and operational disputes.

Here’s how Probe42 adds value!

1. Comprehensive Litigation Coverage:

Probe42 aggregates and standardises data across district courts, tribunals, and regulatory bodies. This ensures organisations have visibility into both high-value financial debt cases and the more frequent but equally critical operational disputes.

2. Early Stress Detection:

Operational defaults are leading indicators of financial instability. By surfacing cases related to vendor and supplier disputes, cheque bounces, or delayed payments, Probe42 enables risk and compliance teams to act before stress turns into insolvency or regulatory action.

3. Sector-Level Insights:

Some industries, manufacturing, real estate, and services, are particularly vulnerable to operational defaults. Probe42 provides benchmarking tools to identify which sectors and entities are most exposed, giving decision-makers a macro and micro view of systemic risk.

4. Entity and Counterparty Risk Profiling:

With Probe42, organisations can assess whether a potential client, borrower, or partner has a history of disputes. By integrating this data into onboarding and credit models, institutions reduce exposure to entities that are consistently involved in operational litigation.

5. Audit-Ready Documentation and Compliance Support:

For teams that need defensible and verifiable information, Probe42 offers structured, audit-ready documentation. This not only strengthens compliance workflows but also ensures regulatory expectations, such as KYB, AML, and credit due diligence, are met with data-backed evidence.

The Road Ahead: Rethinking Debt Recovery Priorities

The rise of operational debt recovery over financial loan recovery is reshaping India’s litigation and recovery landscape. For businesses, lenders, and compliance teams, these disputes are not secondary; they are central to assessing creditworthiness and financial stability.

As operational defaults continue to dominate recovery cases, organisations need data-driven tools to detect risks early, monitor disputes, and make informed decisions. Probe42 empowers risk, compliance, and credit teams with the litigation intelligence needed to stay ahead.

Frequently Asked Questions (FAQs)

1. What is the difference between operational and financial debt?

Financial debt comes from loans or credit facilities, usually owed to banks/NBFCs and filed under IBC Section 7. Operational debt arises from unpaid goods or services, typically filed by suppliers under IBC Section 9.

2. Why are operational debt recovery cases rising faster?

Probe42 data shows 17,376 operational cases vs. 6,954 loan cases. Reasons: delayed vendor payments, cash flow stress, and more SMEs using NCLT Section 9 for recovery.

3. How can companies and lenders track operational debt disputes?

Manual tracking is impractical. Platforms like Probe42 centralise litigation data, enabling real-time monitoring of defaults, sector risk benchmarking, and stronger due diligence.